Investing in DNA synthesis

Downstream products capture the value of improved DNA synthesis tech.

I recently co-authored a technical primer on DNA synthesis with Nima Ronaghi at Breakout Ventures. Together we discussed the history of DNA synthesis, chemical vs. enzymatic synthesis, and compiled a list of early-stage companies working in that space. Ultimately, we synthesized that DNA synthesis is an engineering (and potentially parallelization) problem, not a biological one. With this individual piece, I want to talk a little more about technological specifications and market trends.

‘Vibrant DNA synthesis innovation’ by DALL·E.

Canonical cost vs. quality conundrum

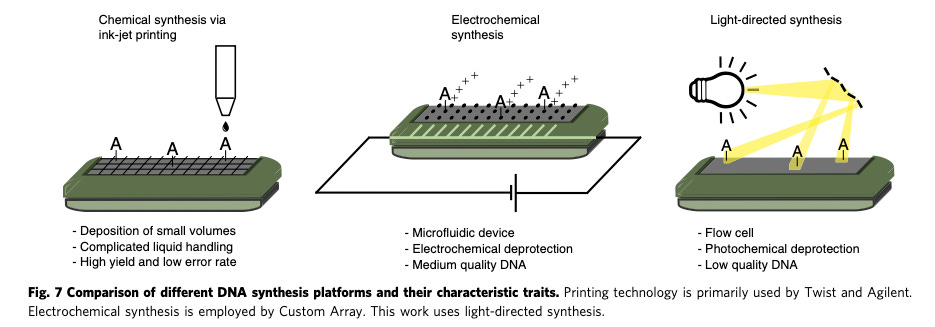

Something not mentioned in the technical primer is the cost and quality tradeoffs. When making an investment in DNA synthesis technologies, knowing the DNA accuracy requirements is absolutely essential. Where therapeutics require near perfect sequence fidelity, oligo pools allow for more sequence variation. Publications such as Antkowiak et al., 2020 do direct comparisons of the different synthesis methods, directly comparing cost and accuracy. Their publication demonstrated 1-2 orders of decreased synthesis cost by using light-directed DNA synthesis. Whereas Twist and Aligent use ink-jet printing and Custom Array (now Genscript) use electrochemical synthesis, light directed synthesis does not use acidic deblocking reagents so is not limited by depurination (as other phosphoramidite chemistries are). This theoretically allows for larger lengths of oligos with light-directed synthesis. However, the absolute length of oligos matter most in highly repetitive regions, or regions with high complementarity. In most cases however, subsequent rounds of PCR, ligation, and/or Gibson assembly can increase the size of DNA fragments. Pooled reactions are particularly time efficient, allowing for the assembly of 1,000 kb fragments over the course of 80 minutes.

To take full advantage of a near-future bioeconomy, the cost of synthetic DNA must drop to a price point where it is no longer a limiting factor in the near-future bioeconomy. Current commercial rates of DNA synthesis are currently between $0.07-0.09/bp, depending on sequence fidelity. Antkowiak et al., 2020 went a step further to compare raw synthesis (not retail costs) with various DNA synthesis techniques, finding its light-directed technique was 1-2 orders of magnitude cheaper ($0.00053/base) than the compared enzymatic, ink-jet, and electrochemical methods. The next cheapest method was deposition-mediatiated phosphoramidite synthesis at $0.00561/base. Antkowiak et al., 2020 ends by stating that increased DNA synthesis parallelization and optimized reagent usage will decrease the per base cost of DNA synthesis to $0.000001, scaling through engineering.

Comparison of multiplexed phosphoramidite synthesis techniques from Antkowiak et al., 2020

Enzymatic synthesis is also priced comparable to ink-jet printing and electrochemical synthesis, but has higher coupling efficiency. However, enzymatic synthesis is not without its foibles, one of which is parallelization. I haven’t been able to find any patents that parallelize enzymatic DNA synthesis, but there have been some publications which parallelize enzymatic DNA synthesis of 12 oligos simultaneously. There is almost certainly multiplexing of to a much larger degree in enzymatic synthesis but it’s unclear if it's been engineered to the magnitude of phosphoramidite synthesis. As mentioned previously, Twist regularly synthesizes 9,600 oligos simultaneously and has patent protection to further parallelize their reactions for the synthesis of 1,000,000 nucleotides simultaneously. This protection suggests their aspirational goal for which their ability has not yet been reported. Despite advances in phosphoramidite and enzymatic DNA synthesis, first strand DNA synthesis remains relatively expensive and time-consuming. In conclusion, parallelization of chemical DNA synthesis has been widely-reported, with enzymatic synthesis lagging behind. Moreover, the canonical fidelity vs. price tradeoffs are apparent in DNA synthesis so this will need to be accounted for in the design of the product, and matched to what is required by the downstream products.

Market trends show where the value lies

Through research on these core areas of technical understanding, I started to see some commercial trends. Because DNA synthesis is difficult and relatively expensive, companies that have some new technology for DNA synthesis and production are ripe for acquisition. Gingko led the way in DNA synthesis deals by acquiring Gen9, which could synthesize 50 gene constructs in the same reaction. In recent years, acquisitions of or exclusive partnerships with DNA synthesis companies has become more frequent.

Genscript acquired Custom Array in 2017 which could synthesize 8 million oligos simultaneously with electrochemical synthesis.

Gigabases’s computer-augmented, multiplexing technology enables Swiss Rockets COVID vaccine company, RocketVax, to quickly make viral particles to fight disease. (Made novel multiplex DNA assembly methodology).

Synhelix was acquired by mRNA producer and CMO, Quantoom Biosciences, as DNA synthesis is essential in the RNA production processes at Quantoom. (Used automated DNA synthesis bioreactor for synthesis of large constructs).

Touchlight signed a deal with Pfizer for exclusive rights to its doggybone (db) DNA synthesis in July 2022.

A Swedish drug discovery company, Biotage, acquired DNA synthesis company ADTbio for ~$55m in 2021.

Although each of the deals are individually beneficial, collectively they sequester useful technologies that could be used for realizing the bioeconomy. For investors though, the acquisition flurry makes investment in new tech all the more interesting because companies that would have been direct formidable competitors (Gen9, Gigabases, SynHelix) aren’t directly in the market. Moreover, the consolidation of DNA synthesis technology by vaccine, cell/gene therapy, and synthetic biology companies demonstrates where the material value lies in DNA synthesis - in downstream products. Even DNA synthesis service companies, like Twist, are trying to capture downstream products via building out DNA storage capabilities. Another trend I’ve seen is that early-stage DNA/RNA synthesis companies are built around therapeutic products: Kano Therapeutics and EnPlusOne Bio work on gene therapy and RNA therapeutics, respectively.

Tying it all together

DNA synthesis companies that don’t work directly on downstream value capture will be acquisition targets by pharma, synthetic biology, or DNA service providers. Therefore, a company that uses DNA synthesis directly towards therapeutics, vaccines or products will create the most value. In the previous article I highlighted the pain points of various types of DNA synthesis and here have concluded that although DNA length is important, the quality and cost are usually an even higher consideration. This is because of the ease of stitching DNA together via Gibson Assembly or ligation reactions. In regard to the enduring debate around phosphoramidite vs. enzymatic synthesis, the honest answer is that it depends on the use-case. For truly decentralized DNA synthesis, ideally enzymatic synthesis would be used as it is less toxic. However, it’s been hard to find instances where enzymatic DNA synthesis is parallelized, especially to the degree of phosphoramidite chemistry (8,000,000+ oligos parallelized with electrochemical synthesis at Custom Array). There is a case to be made where enzymatic synthesis doesn’t need to be parallelized as much due to the longer oligos, but some concerted engineering is still needed for it to be realized. On the other hand, phosphoramidite continues to be engineered to allow for cheaper and longer strand synthesis (e.g. light-directed) but still needs error rate optimization. Ultimately, a company that’s able to do enzymatic synthesis in a highly parallelized way will win with speed of synthesis and accuracy and harmless byproduct. Things to consider are use-cases (which will decide the applicability of enzymatic vs. chemical synthesis) and whether the company is able to capture the downstream value of the cheaper DNA.

There’s still a lot of blank space in DNA synthesis and new companies will continue to emerge as new, non-templated DNA synthesis enzymes and ways of miniaturizing/optimizing synthesis are discovered. As the recent Innovation Endeavors article pointed out, we need to make a lot of stuff, much of which starts with DNA.

We’re incredibly excited about DNA synthesis tech at Compound so do reach out if you’re building here!

Shelby, nice write-up. Please be on the lookout for any new ETF's that develop in the space so that one can spread the risk to a grouping of syn-bio companies instead of individuals having to develop the expertise to make rifle shot selections. Thanks!